A smart payment terminal is a sophisticated hardware device engineered to facilitate secure, automated financial transactions through a diverse array of payment methods, including Near Field Communication (NFC), Quick Response (QR) codes, EMV chip cards, and mobile wallets. These terminals have become ubiquitous across various sectors, such as public transportation, retail environments, institutional cafeterias, automated parking systems, and electronic access control points.

Diverging significantly from traditional Point of Sale (POS) systems, contemporary smart payment terminals function as integrated embedded systems. They seamlessly unify specialized hardware, robust firmware, advanced communication modules, and secure payment processing protocols into a single, cohesive device. This integration allows for greater flexibility, enhanced security, and the ability to operate as part of a broader Internet of Things (IoT) ecosystem.

This comprehensive guide delves into the operational mechanics of smart payment terminals, dissecting their system architecture, detailing their critical components, and outlining the strategic pathways for companies to develop bespoke devices through Original Equipment Manufacturer (OEM) and Original Design Manufacturer (ODM) partnerships.

1. What Is a Smart Payment Terminal?

At its core, a smart payment terminal is an embedded hardware system meticulously designed to perform several critical functions:

• Process Payments Securely: Utilizing encryption and secure elements to protect sensitive financial data during transmission and storage.

• Connect to Cloud or Backend Systems: Maintaining real-time communication with central servers for transaction verification, data logging, and remote management.

• Support Multiple Payment Methods: Offering versatility by accepting contactless cards, QR codes from mobile apps, and traditional chip-and-PIN cards.

• Provide Real-Time Transaction Feedback: Instantly informing the user and the merchant of the transaction status (approved, declined, error).

• Enable Integration with Third-Party Platforms: Allowing seamless connection with inventory management, customer relationship management (CRM), and accounting software.

These versatile terminals are commonly deployed in a variety of demanding environments:

• Public Transport: For rapid bus fare collection and transit gate access.

• Self-Service Kiosks: Enabling unattended purchases in museums, cinemas, or fast-food chains.

• Cafeterias and Food Courts: Facilitating quick meal payments in corporate or educational settings.

• Parking Systems: Automating payment for entry and exit at parking facilities.

• Access Control and Gate Systems: Linking payment to physical entry permissions.

In modern deployments, smart payment terminals are no longer isolated, standalone devices. Instead, they are integral nodes within a connected IoT ecosystem, often running on operating systems like Android to support complex applications and data analytics.

2. Smart Payment Terminal System Architecture

A typical smart payment terminal is built upon a multi-layered architecture where each layer plays a distinct role in ensuring functionality and security.

2.1 Hardware Layer

This is the physical foundation of the device, comprising the tangible components that interact with the user and the environment. It typically includes:

• Main Control Board (MCU or SoC): The brain of the terminal, processing instructions and managing data flow.

• NFC Module: The antenna and chipset responsible for reading contactless payment credentials.

• QR Code Scanner: An optical sensor, often a camera module, for reading 2D barcodes.

• EMV Card Reader: The physical slot and contacts for reading chip cards.

• Communication Modules: Hardware for 4G/LTE, WiFi, Bluetooth, or Ethernet connectivity.

• Power Management System: Regulating voltage and managing battery backup if applicable.

• Display and Input Interface: Screens (LCD/TFT) and physical or virtual keypads for user interaction.

2.2 Firmware Layer

The firmware acts as the intermediary between the hardware and the high-level software. It ensures:

• Device Boot and Operation: Initializing hardware components upon startup.

• Peripheral Communication: Managing the data exchange between the CPU and modules like the NFC reader or printer.

• Payment Protocol Handling: Executing the low-level logic required by payment networks (e.g., ISO 8583).

• Security Enforcement: Implementing hardware-level security measures and tamper detection.

2.3 Application Layer

This layer handles the user-facing logic and business rules:

• User Interface (UI/UX): The visual elements and navigation flow presented to the customer and cashier.

• Payment Workflows: Orchestrating the steps from item selection to payment confirmation.

• Transaction Processing Logic: Calculating totals, taxes, and discounts.

• Integration with Cloud Systems: Formatting data for API calls to the backend.

2.4 Cloud / Backend Layer

The remote infrastructure that supports the terminal:

• Transaction Processing: The payment gateway that communicates with banks and card networks.

• Data Analytics: Aggregating sales data for business intelligence.

• Remote Device Management: Monitoring device health, status, and location.

• System Updates (OTA): Pushing firmware and software updates over the air to fix bugs or add features.

3. Key Components of a Smart Payment Terminal

Understanding the granular components is essential for anyone looking to develop or customize these devices.

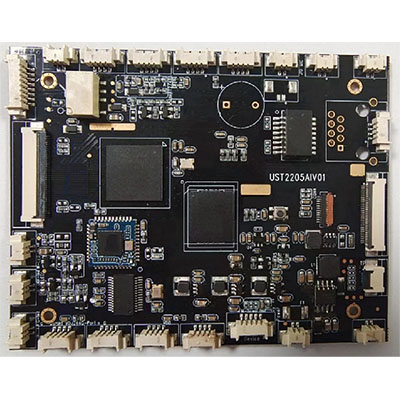

3.1 Main Control Board (Core Board)

The most critical part of the device is the main control board. It houses the processor, memory, and essential interfaces.

• CPU / MCU / SoC: High-performance processors (often ARM-based) capable of running modern operating systems like Android or Linux.

• Memory (RAM + Flash): Sufficient storage for the OS, applications, and transaction logs.

• Peripheral Interfaces: USB, UART, SPI, and I2C ports to connect various modules.

• System Control Logic: Managing power distribution and system resets.

This is the primary focus area for embedded hardware solution providers, who design these boards to be robust and versatile.

3.2 Payment Modules

These are the specialized components that interact with payment instruments:

• NFC Module: Supports standards like Mifare, DESFire, and payment network contactless specifications.

• EMV Card Reader: Must be L1 and L2 certified to ensure compatibility with global chip card standards.

• QR Scanner: High-resolution cameras or dedicated scan engines capable of reading screens in various lighting conditions.

These modules must comply with rigorous international payment standards such as EMVCo and PCI PTS to ensure interoperability and security.

3.3 Communication Modules

Reliable connectivity is non-negotiable for real-time payments:

• 4G / LTE Modules: Ensuring connectivity in mobile environments or areas without WiFi.

• WiFi / Bluetooth: For standard internet access and peripheral pairing (e.g., handheld terminals).

• Ethernet: For stable, high-speed connections in fixed retail locations.

3.4 Security Components

Security is the backbone of any payment device. Key components include:

• Secure Element (SE) Chips: Dedicated hardware for storing encryption keys and performing cryptographic operations.

• Encryption Modules: Hardware accelerators for algorithms like AES and RSA.

• Tamper Detection: Sensors that wipe sensitive data if the device casing is breached.

• Secure Boot: Ensuring the device only runs authenticated software.

3.5 Human-Machine Interface (HMI)

The HMI facilitates interaction:

• Touchscreen or LCD Display: High-brightness, durable screens (often capacitive touch) that can withstand heavy use.

• Buttons or Keypad: Physical keys, often including a secure PIN pad for entering passwords.

• LED Indicators: Visual cues for status (e.g., "Ready," "Processing," "Error").

• Audio Output: Speakers or buzzers for voice prompts and beep feedback.

4. How Smart Payment Terminals Process Transactions

The journey of a transaction through a smart payment terminal is a complex ballet of hardware and software interactions:

1. User Initiates Payment: The customer presents their payment method—tapping a card (NFC), scanning a QR code, or inserting a chip card.

2. Terminal Captures Data: The specific module (NFC reader, camera, or card slot) reads the encrypted payment credentials.

3. Data Encryption: The terminal's Secure Element immediately encrypts this sensitive data to prevent interception.

4. Transmission to Backend: The encrypted payload is sent via the communication module (4G/WiFi) to the payment gateway or acquirer.

5. Gateway Processing: The payment gateway routes the request to the relevant card network (Visa, Mastercard, UnionPay) and then to the issuing bank.

6. Authorization Response: The bank verifies funds and fraud checks, then sends an approval or decline code back through the chain.

7. Terminal Feedback: The terminal receives the response and displays the result (Success/Failure) on the screen, often accompanied by a sound.

8. Logging: The transaction details are stored locally on the device and synced with the cloud system for record-keeping.

5. OEM vs ODM in Smart Payment Terminal Development

For companies looking to enter the market or upgrade their hardware, understanding the distinction between OEM and ODM is vital.

OEM (Original Equipment Manufacturer)

In an OEM arrangement:

• You Provide the Design: The client company creates the detailed specifications, schematics, and industrial design.

• Manufacturer Produces: The factory builds the hardware exactly to your blueprints.

• Pros & Cons: This offers maximum control over the product's look and feel but requires significant in-house R&D capability and resources.

ODM (Original Design Manufacturer)

In an ODM arrangement:

• Supplier Provides Design: The manufacturer offers pre-existing designs and hardware platforms that can be rebranded or slightly modified.

• Faster Time-to-Market: Since the R&D is largely done, products can be launched much quicker.

• Ideal Scenario: This is perfect for companies that excel in software or sales but lack the internal hardware engineering teams to build a terminal from scratch.

Many global companies rely on ODM partners to develop embedded boards and hardware systems, allowing them to focus on their core competencies like software development and market expansion.

6. Custom Embedded Board Development for Payment Terminals

For companies without extensive internal R&D departments, custom embedded board development represents the most efficient path to a proprietary product.

Key Benefits

• Faster Product Development: Leveraging existing reference designs accelerates the timeline.

• Lower R&D Cost: Reduces the need for hiring large teams of electrical and firmware engineers.

• Flexible Customization: Boards can be tailored to specific needs (e.g., specific port layouts or module integrations).

• Scalable Production: Partners handle the supply chain and manufacturing scaling.

• Reduced Technical Risk: Proven designs minimize the chance of hardware failures.

Customization Options

Partners can customize various aspects of the board:

• Hardware Interfaces: Adding or removing USB, RS232, or GPIO ports.

• Communication Modules: Selecting specific 4G bands or WiFi standards.

• Payment Integration: Integrating specific NFC chips or secure elements.

• Power Design: Optimizing for battery life or specific voltage inputs.

• Form Factor: Adjusting the physical size and shape of the PCB to fit unique enclosures.

This is where embedded hardware solution providers play a critical role—delivering ready-to-integrate core boards that clients can directly use in their own devices, significantly lowering the barrier to entry.

7. Industry Applications

Smart payment terminals are versatile tools used across a spectrum of industries, each with unique requirements.

Transportation

In the transit sector, speed and durability are paramount. Terminals are used for:

• Bus Fare Collection: Ruggedized units that handle vibrations and temperature changes.

• Smart Ticketing: Validating digital passes and contactless cards at turnstiles.

• Transit Access Control: Integrating payment with physical gate opening mechanisms.

Cafeteria & Food Service

In high-volume food service, efficiency is key. Applications include:

• Meal Payment Systems: Fast transaction times to reduce lunch queues.

• Self-Service Ordering Kiosks: Allowing customers to order and pay without staff intervention.

• Nutritional Displays: Advanced terminals can show calorie counts and nutritional info on the customer screen.

️ Parking & Access Control

These systems require robust outdoor connectivity:

• Parking Payment Systems: Pay-on-foot kiosks or barrier-integrated readers.

• Gate Control Systems: Linking payment validation directly to the barrier arm.

Retail & POS

The traditional retail space is evolving:

• Smart POS Systems: Android-based terminals that run third-party apps for inventory and loyalty management.

• Self-Service Checkout: Allowing shoppers to scan and pay simultaneously.

8. How to Choose a Smart Payment Hardware Supplier

Selecting the right partner is crucial for the success of your hardware project. When evaluating a supplier for embedded boards or terminal development, consider the following criteria:

• Hardware R&D Capability: Do they have a proven track record of designing stable, high-performance boards?

• Firmware Development Expertise: Can they provide the necessary drivers and SDKs for your software team?

• Industry Experience: Have they worked on payment systems before? Do they understand EMV and PCI requirements?

• Compliance: Can their hardware pass FCC, CE, and EMV certifications?

• Customization Flexibility: Are they willing to tweak the design to fit your specific needs?

• Production Capacity: Can they scale from prototype to mass production efficiently?

A strong supplier should provide end-to-end support from design to production, acting as a true partner rather than just a vendor.

9. Future Trends in Smart Payment Terminals

The landscape of payment hardware is shifting rapidly, driven by technological advancements and changing consumer behaviors.

• AI-Powered Transaction Analysis: Terminals are beginning to use AI to detect fraud in real-time or offer personalized upsells based on purchase history.

• Cloud-Based Device Management: As fleets of devices grow, managing them remotely via the cloud (updating software, monitoring health) becomes essential.

• Biometric Authentication: Integration of fingerprint scanners and facial recognition cameras is making payments more secure and password-free.

• Multi-Payment Integration: Future terminals will support an even wider array of payment options, including cryptocurrencies and central bank digital currencies (CBDCs).

• IoT Ecosystem Integration: Terminals will communicate more deeply with other smart devices, such as smart shelves in retail or kitchen displays in restaurants.

Smart payment terminals are becoming more intelligent, connected, and secure, evolving from simple payment acceptors into comprehensive business management tools.

10. Frequently Asked Questions (FAQ)

Q1: What is the difference between a POS system and a smart payment terminal?

A POS system is typically a broader setup that may include a PC or tablet running software, whereas a smart payment terminal is a dedicated, all-in-one embedded hardware device that integrates payment modules, communication systems, and often the user interface into a single unit.

Q2: Can I customize a smart payment terminal?

Yes. Through OEM or ODM development, you can customize the hardware specifications, firmware features, industrial design (appearance), and software functionality to match your brand and operational needs.

Q3: How long does it take to develop a custom payment terminal?

The timeline depends on the complexity of the customization. However, for standard hardware development and testing using existing core boards, it typically takes 2–6 months. Full custom designs may take longer.

Q4: What payment methods are supported?

Modern smart terminals are designed to be versatile. Common methods include NFC (contactless), QR codes (Alipay, WeChat Pay, etc.), EMV chip cards (insert), and magnetic stripe cards (swipe), as well as mobile wallets like Apple Pay and Google Pay.

Q5: Do I need hardware R&D to launch a product?

Not necessarily. By working with a capable embedded hardware solution provider or ODM, you can leverage their existing designs and expertise. This allows you to focus on branding, software, and market development without needing to build a hardware engineering team from scratch.

Conclusion

Smart payment terminals are the linchpin of modern digital payment infrastructure, enabling secure, rapid, and scalable transactions across a myriad of industries. They bridge the gap between physical commerce and digital finance.

For companies lacking in-house R&D capabilities, the strategic move is to partner with a specialized embedded hardware and core board provider. This approach not only accelerates time-to-market but also ensures that the device is built on a foundation of proven technology and expertise.

About Us

We are a premier provider of custom embedded core board development and smart terminal solutions. We empower businesses to innovate by building:

• Smart Payment Terminals: Secure, fast, and versatile.

• Transportation Payment Systems: Rugged and reliable.

• Cafeteria and POS Devices: User-friendly and efficient.

• Access Control and Kiosk Systems: Integrated and smart.